3.1 Managing Your Money

Stevy Scarbrough

Learning Objectives

Upon completion of this reading, you will be able to:

- Develop financial literacy skills to prepare for your financial future

- Establish financial goals

- Identify strategies for creating and maintaining a budget

- Describe the benefits and risks of credit

This chapter offers you insight into your finances so that you can make good decisions and avoid costly mistakes. We all experience opportunities to spend money and try to get what we want. Many think only about now and not next month, next year, or ten years from now, but our behavior now has consequences later. Not everyone will own all the latest technology, drive their dream car, continually invest for their retirement, or live in their dream home. But by understanding the different components of earning money, banking, credit, and budgeting, you can begin working toward your personal and financial goals. We’ll also discuss a related topic, safeguarding your accounts and personal information, which is critical to protecting everything you’ve worked for.

Budgets

Map your financial path using a spending and savings plan, or budget, which tracks your income, savings, and spending. You check on your progress using a balance sheet that lists your assets, or what you own, and your liabilities, or what you owe. A balance sheet is like a snapshot, a moment in time, that you will use to check your progress.

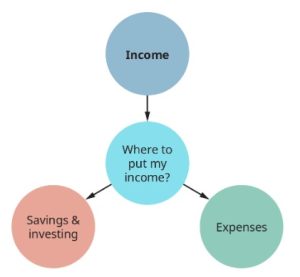

Budgeting is unpleasant to some people because it just looks like work. But who will care more about your money than you? We all want to know if we have enough money to pay our bills, travel, get an education, buy a car, etc. Technically, a budget is a specific financial plan for a specified time. Budgets have three elements: income, saving and investing, and expenses.

Income

Income most often comes from our jobs in the form of a paper or electronic paycheck. When listing your income for your monthly budget, you should use your net pay, also called your disposable income. It is the only money you can use to pay bills. If you currently have a job, look at the pay stub or statement. You will find your gross pay, the total amount of money you earned, then some money deducted for a variety of taxes, leaving a smaller amount—your net pay, the actual take home earning you have to cover your expenses and/or set aside. Sometimes you have the opportunity to have some other, optional deductions taken from your paycheck before you get your net pay. Examples of optional deductions include 401(k) or health insurance payments. You can change these amounts, but you should still use your net pay when considering your budget.

Some individuals receive disability income, social security income, investment income, alimony, child support, and other forms of payment on a regular basis. All of these go under income. During school, you may receive support from family that could be considered income. You may also receive scholarships, grants, or student loan money.

Saving and Investing

The first bill you should pay is to yourself. You owe yourself today and tomorrow. That means you should set aside a certain amount of money for savings and investments, before paying bills and making discretionary, or optional, purchases. Savings can be for an emergency fund or for short-term goals such as education, a wedding, travel, or a car. Investing, such as putting your money into stocks, bonds, or real estate, offers higher returns at a higher risk than money saved in a bank. Investments include retirement accounts that can be automatically funded with money deducted from your paycheck. Automatic payroll deductions are an effective way to save money before you can get your hands on it. Setting saving as a priority assures that you will work to make the payment to yourself as hard as you work to make your car or housing payment. The money you “pay” toward saving or investing will earn you back your money, plus some money earned on your money. Compare this to the cost of buying an item on credit and paying your money plus interest to a creditor. Paying yourself first is a habit that pays off!

Expenses

Expenses are categorized in two ways. One method separates them into fixed expenses and variable expenses. Rent, insurance costs, and utilities (power, water) are fixed: they cost about the same every month and are predictable based on your arrangement with the provider. Variable expenses, on the other hand, change based on your priorities and available funds; they include groceries, restaurants, cell phone plans, gas, clothing, and so on. You have a good degree of control over your variable expenses. You can begin organizing your expenses by categorizing each one as either fixed or variable.

A second way to categorize expenses is to identify them as either needs or wants. Your needs come first: food, basic clothing, safe housing, medical care, and water. Your wants come afterward, if you can afford them while sticking to a savings plan. Wants may include meals at a restaurant, designer clothes, video games, other forms of entertainment, or a new car. After you identify an item as a need or want, you must exercise self-control to avoid caving to your desire for too many wants.

Balancing Your Budget

Would you take all your cash outside and throw it up in the air on a windy day? Probably not. We want to hold on to every cent and decide where we want it to go. Our budget allows us to find a place for each dollar. We should not regularly have money left over. If we do, we should consider increasing our saving and investing. We also should not have a negative balance, meaning we don’t have enough to pay our bills. If we are short of money, we can look at all three categories of our budget: income, savings, and expenses.

We could increase our income by taking a second job or working overtime, although this is rarely advisable alongside college coursework. The time commitment quickly becomes overwhelming. Another option is to cut savings, or there’s always the possibility of reducing expenses. Any of these options in combination can work.

Another, even less desirable option is to take on debt to make up the shortfall. This is usually only a short-term solution that makes future months and cash shortages worse as we pay off the debt. When we budget for each successive month, we can look at what we actually spent the month before and make adjustments.

Tracking the Big Picture

When you think about becoming more financially secure, you’re usually considering your net worth, or the total measure of your wealth. Earnings, savings, and investments build up your assets—that is, the valuable things you own. Borrowed money, or debt, increases your liabilities, or what you owe. If you subtract what you owe from what you own, the result is your net worth. Your goal is to own more than you owe.

When people first get out of college and have student debt, they often owe more than they own. But over time and with good financial strategies, they can reverse that situation. You can track information about your assets, liabilities, and net worth on a balance sheet or part of a personal financial statement. This information will be required to get a home loan or other types of loans. For your net worth to grow in a positive direction, you must increase your assets and decrease your liabilities over time.

Assets (Owned) – Liabilities (Owed) = Net Worth

Good practices that build your wealth include tracking all of your spending and saving, knowing the difference between your needs and your wants, and resisting impulse buying and emotional spending. Negative practices that can lead you into further debt include living paycheck to paycheck with no plan, spending money on your wants instead of saving, and using credit to buy things you don’t need, increasing what you owe.

You can write down your budget on paper or using a computer spreadsheet program such as Excel, or you can find popular budgeting apps that work for you (Depra, 2015). Some apps link to your accounts and offer other services such as tracking credit cards and your credit score. The key is to find an app that does what you need and use it.

Here are some examples:

Emergency Funds

Plan on the unplanned happening to you. It happens to all of us: a car repair, a broken computer, an unplanned visit to the doctor, a friend or relative in desperate need, etc. How will you pay for it? A recent study found that over 60 percent of households could not pay cash for a $400 unexpected expense (Board of Governors of the Federal Reserve System, 2019). Could you?

What Is an Emergency Fund?

An emergency fund is a cash reserve that’s specifically set aside for unplanned expenses or financial emergencies (Consumer Financial Protection Bureau, n.d.) Some common examples include car repairs, home repairs, medical bills, and a loss of income. In general, emergency savings can be used for large or small unplanned bills or payments that are not part of your routine monthly expenses and spending.

Why Do I Need an Emergency Fund?

Without savings, even a minor financial shock could set you back, and if it turns into debt, it can potentially have a lasting impact. Research suggests that individuals who struggle to recover from a financial shock have less savings to help protect against a future emergency. They may rely on credit cards or loans, which can lead to debt that’s generally harder to pay off. They may also pull from other savings, such as retirement funds, to cover these costs.

How Much Money Should I Keep in My Emergency Fund?

There is no magic or “official” amount to keep in an emergency fund, but you can look at your own life to get an idea to start with. How much could you put into a bank account to have for emergencies? Some students and their parents will not have a problem paying for most emergencies, but many students are on their own. What can you save up over time? A common recommendation for graduates with full-time jobs is perhaps three to six months’ worth of expenses. This may not be practical for you. A large sampling of students in financial literacy classes recommend approximately $1,000.

One thousand dollars can cover a lot of small to medium unexpected expenses, such as last-minute textbooks, computer repair or replacement, car repair, or a prescription or doctor’s visit. The emergency fund is best kept separate from other money for living expenses to protect it as emergency money. While you could keep cash, an emergency fund is often best kept in a bank, in order to avoid theft or loss and still have easy access by debit card or ATM. Pizza is not an emergency!

How Do I Create an Emergency Fund?

Emergency funds can be created quickly if you have the money, or over time if you need to save a little from each paycheck, loan, or gift. You can use a financial planning tool similar to the one in section 10.1. Follow these steps:

- Set an emergency fund goal.

- Identify an amount to keep on hand.

- Determine how to fund it, monthly or all at once.

- Decide where you will keep your fund (e.g., a savings account), and set specific dates to deposit money in it.

- Start now!

Safety and Success: Bank on It!

The banking system in the United States is one of the safest and most regulated banking systems in the world. A host of federal and state agencies regulate financial institutions to keep them from accidentally or purposefully losing customer money.

Banks, Credit Unions, and Online Banking

In the United States, financial institutions (FIs) are divided into multiple types of companies. The banking system is generally divided into banks and credit unions, which have similar offerings and are both regulated and insured by the federal government.

Choosing a Bank or Credit Union

When choosing a bank or credit union, it is important to understand what you are looking for and what benefits each company provides. Generally, large national banks offer the most advanced technology and a large network of branches. There are also smaller community banks that serve specific groups of people and may offer products to meet the specific needs of the community. For example, a community bank that serves Latino customers might make it easier to send money to family in South American countries, while a bank that focuses on small businesses will promote products specifically needed by business owners.

Credit unions differ from banks in that they don’t have a profit motive. Instead, they are not-for-profit organizations that are owned by the people who bank with them. Each member of a credit union gets one vote for the board of directors, which runs the credit union. This means that whether you have $5 in your account or $5 million, you get the same vote. Credit unions tend to offer better rates and lower fees, on average, than banks.

There is no single best answer for what bank or credit union you should choose. The most vital question to ask and answer about a financial institution is whether it meets both your current and your future needs. Use figure 10.3 to compare different options and determine the best one for you.

Many banks and credit unions do not publish the interest rates paid on deposit accounts or charged on loans. While some colleges have their own bank or credit union right on campus, you should consider visiting at least one other bank or one credit union to compare. You may also explore at least one online bank, which will publish interest rates on their website. Consider interest rates, access to automated teller machines (ATMs), online transfers, automatic paycheck deposits, branch locations if you will use one, and other services important to you. Since you will select a bank or credit union that is insured, do not feel pressure to use any specific institution.

Banking Products and Services

Banks and credit unions offer a similar set of financial products or services, called account types. The difference between the account types lies primarily in how easy it is to put money into or take money out of an account. Regulations set maximum numbers of transactions (deposits or withdrawals) for each type of account at a bank or credit union.

How you use these accounts is less about the rules and more about how long you plan to keep the money in the account. The main reason to use a bank is to keep your money safe and available. Banks may offer other services that benefit you, such as certificates of deposit (which allow you to earn higher interest over a longer time), retirement accounts, and car and home loans.

Checking

Checking accounts allow you to deposit money and take money out anytime you want. There are no government limits on the number of transactions, although a bank or credit union might begin to charge you if you make too many transactions. Checking accounts often don’t pay any interest or pay an extremely low rate of interest. They are used to keep money safe and pay bills conveniently.

Checking accounts are ideal for depositing paychecks, cashing paper checks, buying everyday items, and paying your bills. The money you have in your checking account should be money you plan to spend by the end of the month. Any money you don’t plan to spend within a month should be transferred from your checking account to a savings account. Your savings account should be the first bill that you pay each month. You can still add extra at the end of the month!

Savings Accounts

Savings accounts allow you a specific number of transactions each month or each quarter. If you go over the maximum number of transactions, the bank won’t let you take any more money out or put any more money into the account until the next month. Savings accounts pay a small amount of interest on your money, but usually not enough to keep up with inflation or overcome banking fees (see below).

This actually causes your savings to go backwards. If you earn 2 percent on a savings account but inflation is 3 percent per year, you are losing 1 percent of purchasing power each year. For this reason, money in a savings account should be money you plan to spend within the next 12–48 months. The only exception to this is money you have saved for an emergency, called an emergency fund. Since you never know when an emergency (such as losing your job) is going to happen, you want the money to be available to you in a savings account.

Debit Cards

When you get a checking account, you’ll also get a debit card, or check card. This card allows you to access the money in your checking account (and savings account at an ATM) using a plastic card similar to a credit card. But it is not a credit card.

A debit card only uses money available in your account. Paying with a debit card is like paying with a paper check, but more immediate and convenient. You will have the option of selecting overdraft protection, which means the bank or credit union will allow you to buy stuff even if you don’t have enough money in your account; they’ll just charge you a fee, perhaps $25, for each event. This can be compared to a high-interest loan. Depending on how many things you buy in a week, overdraft protection could add many fees to your statement and use up your cash so it will not be available for your planned expenses. Consider opting out of overdraft protection and carefully keeping track of your account balance. This way you can only spend the money that you have.

Be aware that by using your debit card at an ATM associated with a different bank, you can incur fees—sometimes from both banks!

Debit cards offer a lot of security benefits over carrying around cash, including the ability to cancel a lost or stolen debit card. While the legal protections on debit cards are not as great as the legal protections on credit cards, you can’t go into debt using a debit card. This inability to go into significant debt is a major advantage for those who struggle with debt.

Banking Fees

Banks and credit unions charge fees to operate. Many charge fees for a checking or savings account, overdrafts, and other services. You should seek to avoid fees for which you receive no extra services or when you can get similar services elsewhere for free. Two areas that are most subject to fees are services and “triggered” events. Triggered events are primarily caused by actions such as overdrawing your account (an overdraft). Overdraft fees are avoidable. The best way to avoid an overdraft fee is to continually monitor your bank balance and only spend money that you have.

Standard bank fees can often be avoided by taking one or more measures as specified by the bank, such as maintaining a minimum balance or using direct deposit. Avoid getting paid on a payroll or prepaid card unless you know all related costs or have a reason to want to be paid in that manner. Payroll cards often lead to ATM and banking fees, so federal law requires employers to offer you an alternative (Johnson, 2021). Ask at your financial institution for assistance in setting up an account or accounts that are best for you.

The Danger of Debt

When you take out a loan, you take on an obligation to pay the money back, with interest, through a monthly payment. You will take this debt with you when you apply for auto loans or home loans, when you enter into a marriage, and so on. Effectively, you have committed your future income to the loan. While this can be a good idea with student loans, take on too many loans and your future self will be poor, no matter how much money you make. Worse, you’ll be transferring more and more of your money to the bank through interest payments.

Compounding Interest

While compounding works to make you money when you are earning interest on savings or investments, it works against you when you are paying the interest on loans. To avoid compounding interest on loans, make sure your payments are at least enough to cover the interest charged each month. The good news is that the interest you are charged will be listed each month on the loan account statements you are sent by the bank or credit union, and fully amortized loans will always cover the interest costs plus enough principal to pay off what you owe by the end of the loan term.

The two most common loans on which people get stuck paying compounding interest are credit cards and student loans. Paying the minimum payment each month on a credit card will just barely cover the interest charged that month, while anything you buy with the credit card will begin to accrue interest on the day you make the purchase. Since credit cards charge interest daily, you’ll begin paying interest on the interest immediately, starting the compound interest snowball working against you. When you get a credit card, always pay the credit card balance down to $0 each month to avoid the compound interest trap.

Student loans are another way you can be caught in the compound interest trap. When you have an unsubsidized student loan or put your loans into deferment, the interest continues to rack up on the loans. Again, you’ll be charged interest on the interest, not just on the original loan amount, forcing you to pay compound interest on the loan.

Sacrificing Your Future Fun

When you graduate college, you are most likely to graduate with student loan debt and credit card debt (Fay, 2023). Many students use credit cards and student loans to allow them to pay for fun today, such as trips, clothing, and expensive meals.

Getting into debt while in college forces you to sacrifice your future fun. Say you take out $100,000 in student loans instead of the $50,000 you need, doubling your monthly payment. You are not just making an extra $338 payment; you are also sacrificing anything else you can do with that money. You sacrifice that extra $338 a month, every month, for the next twenty-five years. You can’t use it to go to the movies, pay down other debt, save for a home, take a vacation, or throw a party. When you sign those papers, you sacrifice all those opportunities every month for decades. As a result, when you take out a loan, you should make sure it’s a good loan.

How Much Good Debt to Take On

A drink of water is refreshing on a hot day and is required to stay alive. Too much water, however, and you will drown.

During college and for the first few years after graduation, most students should only have two loans: student loans and possibly a car loan. We’ve already discussed your student loans, which should be equal to or less than your first year’s expected salary after graduation.

When you get a car, you should keep your car payment to between 10 and 20 percent of your monthly take-home pay. This means if your paycheck is $200 per week, your car payment should be no more than $80–$160 each month.

In total, you want your debt payments (plus rent if you are renting) to be no more than 44 percent of your take-home pay. If you are planning to build wealth, however, you want to cap it at 30 percent of take-home pay.

Signs You Have Too Much Debt

You can consider yourself in too much debt if you have any of the following situations:

- You cannot make your minimum credit card payments.

- Your money is gone before your next paycheck.

- Bill collectors are contacting you.

- You are unable to get a loan.

- Your paycheck is being garnished by creditor.

- You are considering a debt consolidation loan with extra fees added.

- Your items are repossessed.

- You do not know your debt or financial situation.

Getting and Using a Credit Card

One of the most controversial aspects of personal finance is the use of credit cards. While credit cards can be an incredibly useful tool, their high interest rates, combined with the how easily credit cards can bury you in debt, make them extremely dangerous if not managed correctly.

There are three main benefits of getting a credit card. The first is that credit cards offer a secure and convenient method of making purchases, similar to using a debit card. When you carry cash, you have the potential of having the money lost or stolen. A credit card or debit card, on the other hand, can be canceled and replaced at no cost to you.

Additionally, credit cards offer greater consumer protections than debit cards do. These consumer protections are written into law, and with credit cards you have a maximum liability of $50. With a debit card, you are responsible for transfers made up until the point you report the card stolen. In order to have the same protections as with credit cards, you need to report the card lost or stolen within 48 hours. The longer you wait to report the loss of the card, or the longer it takes you to realize you lost your card, the more money you may be responsible for, up to an unlimited amount (Federal Trade Commission, 2022).

The final benefit is that a credit card will allow you to build your credit score, which is helpful in many aspects of life. While most people associate a credit score with getting better rates on loans, credit scores are also important to getting a job, lowering car insurance rates, and finding an apartment (Troesh, 2016).

What Is a Good Credit Score?

Most credit scores have a 300–850 score range. The higher the score, the lower the risk to lenders. A “good” credit score is considered to be in the 670–739 score range.

| Credit Score Ranges | Rating | Description |

| <580 | Poor | This credit score is well below the average score of US consumers and demonstrates to lenders that the borrower may be a risk. |

| 580-669 | Fair | This credit score is below the average score of US consumers, though many lenders will approve loans with this score. |

| 670-739 | Good | This credit score near or slightly above the average of US consumers, and most lenders consider this good score. |

| 740-799 | Very Good | This credit score is well above the average of US consumers and demonstrates to lenders that the borrower is very dependable. |

| 800+ | Exceptional | This credit score is well above the average score of US consumers and clearly demonstrates to lenders that the borrower is an exceptionally low risk. |

Components of a Credit Score and How to Improve Your Credit

Credit scores contain a total of five components. These components are credit payment history (35 percent), credit utilization (30 percent), length of credit history (15 percent), new credit (10 percent), and credit mix (10 percent). The main action you can take to improve your credit score is to stop charging and pay all bills on time. Even if you cannot pay the full amount of the credit card balance, which is the best practice, pay the minimum on time. Paying more is better for your debt load but does not improve your score. Carrying a balance on a credit card does not improve your score. Your score will go down if you pay bills late and owe more than 30 percent of your credit available. Your credit score is a reflection of your willingness and ability to do what you say you will do—pay your debts on time.

How to Use a Credit Card

All the benefits of credit cards are destroyed if you carry credit card debt. Credit cards should be used as a method of paying for things you can afford, meaning you should only use a credit card if the money is already sitting in your bank account and is budgeted for the item you are buying. If you use credit cards as a loan, you are losing the game.

Every month, you should pay your credit card off in full, meaning you will be bringing the loan amount down to $0. If your statement says you charged $432.56 that month, make sure you can pay off all $432.56. If you do this, you won’t pay any interest on the credit card.

But what happens if you don’t pay it off in full? If you are even one cent short on the payment, meaning you pay $432.55 instead, you must pay daily interest on the entire amount from the date you made the purchases. Your credit card company, of course, will be perfectly happy for you to make smaller payments—that’s how they make money. It is not uncommon for people to pay twice as much as the amount purchased and take years to pay off a credit card when they only pay the minimum payment each month.

What to Look for in Your Initial Credit Card

-

Find a Low-Rate Credit Card

Even though you plan to never pay interest, mistakes will happen, and you don’t want to be paying high interest while you fix a misstep. Start by narrowing the hundreds of card options to the few with the lowest APR (annual percentage rate).

-

Avoid Cards with Annual Fees or Minimum Usage Requirements

Your first credit card should ideally be one you can keep forever, but that’s expensive to do if they charge you an annual fee or have other requirements just for having the card. There are many options that won’t require you to spend a minimum amount each month and won’t charge you an annual fee.

-

Keep the Credit Limit Equal to Two Weeks’ Take-Home Pay

Even though you want to pay your credit card off in full, most people will max out their credit cards once or twice while they are building their good financial habits. If this happens to you, having a small credit limit makes that mistake a small mistake instead of a $5,000 mistake.

-

Avoid Rewards Cards

Everyone loves to talk about rewards cards, but credit card companies wouldn’t offer rewards if they didn’t earn them a profit. Rewards systems with credit cards are designed by experts to get you to spend more money and pay more interest than you otherwise would. Until you build a strong habit of paying off your card in full each month, don’t step into their trap.

Attributions

College Success Author: Amy Baldwin Provided by: OpenStax Located at: https://openstax.org/details/books/college-success License: CC BY 4.0

College Success. Author: Amber Gilewski. Provided by: Lumen Learning. Located at: https://courses.lumenlearning.com/wm-collegesuccess-2/chapter/text-causes-of-stress/ License: CC BY: Attribution

References

Board of Governors of the Federal Reserve System. (2019, May). Report on the Economic Wellbeing of US Households. Retrieved from https://www.federalreserve.gov/publications/2019-economic-well-being-of-us-households-in-2018-dealing-with-unexpected-expenses.htm

Consumer Financial Protection Bureau. (n.d.). An essential guide to building an emergency fund. Retrieved from https://www.consumerfinance.gov/an-essential-guide-to-building-an-emergency-fund/

Depra, D. (2015, September 2). Best budgeting apps for college students: Mint, You Need a Budget and more. Tech Times. Retrieved from http://www.techtimes.com/articles/80726/20150902/best-budgeting-apps-for-college-students-mint-you-need-a-budget-and-more.htm

Fay, B. (2023, July 21). Demographics of Debt. Debt.org. Retrieved from https://www.debt.org/faqs/americans-in-debt/demographics/

Federal Trade Commission. (2022, January). Lost Or stolen credit, ATM, and debit cards. Federal Trade Commission Consumer Advice. Retrieved from https://consumer.ftc.gov/articles/lost-or-stolen-credit-atm-debit-cards#:~:text=Go%20to%20ReportFraud.ftc.gov,easy%20for%20you%20to%20report.

Johnson, H. (2021, February 26). It pays to know these five things about payroll cards. Credit Cards.com. Retrieved from https://www.creditcards.com/credit-management/payroll_cards-fees-employer-1271/

Troesh, J. E. (2016, August 25). Four surprising ways your credit score will affect your life. Purposeful Finance. Retrieved from https://www.purposefulfinance.org/home/Articles/2016/four-surprising-ways-your-credit-score-will-affect-your-life